Save or Spend Calculator

Feel stuck every time you think about spending?

See what your money really costs in time and income—before you decide.

Get a clearer perspective and make money decisions you can feel good about.

Why Every Spending Decision Has a Hidden Cost

Every purchase has two price tags: the money you pay today and the time it took you to earn it. When you look at spending through both lenses, decisions get clearer fast—because you’re no longer asking, “Can I afford this?” You’re asking, “Is this worth the hours of my life?”

That’s the idea behind the Save or Spend Calculator. It helps you pause and translate a purchase into something real: effort and time. If you earn $20 per hour and an item costs $200, that purchase represents about 10 hours of work(before factoring in taxes and other costs). Seeing the “time cost” can be a powerful reality check.

There’s also the hidden cost most people don’t consider: what that money could have done instead. If you don’t spend it, you might save it for a goal, build an emergency buffer, pay down debt, or invest for future growth. That doesn’t mean spending is bad—it means spending has trade-offs. The calculator is designed to make those trade-offs easier to see.

This tool is especially helpful for “medium” purchases—the ones that aren’t huge enough to trigger serious planning, but big enough to slow your progress. Things like upgrades, subscriptions, impulse buys, or “treat yourself” spending can quietly add up over time. When you step back and see the bigger picture, you can decide more intentionally.

Use the calculator when you feel stuck between spending now and saving for later. It’s not here to judge you or tell you what to do. It’s here to give you a clearer perspective—so your choices match your priorities.

How the Save or Spend Calculator Works

The Save or Spend Calculator works by analyzing the relationship between your income and the cost of a purchase. After entering your income and the expense amount, the tool estimates:

-

How many hours of work the purchase represents

-

The short-term impact on your available income

-

The long-term opportunity cost of spending versus saving

For example, if you earn $30 per hour and want to buy a $300 item, that purchase represents approximately 10 hours of work. Seeing the cost in time can often change how a spending decision feels.

For a detailed breakdown of the formula and methodology, visit our full explanation on the How It Works page.

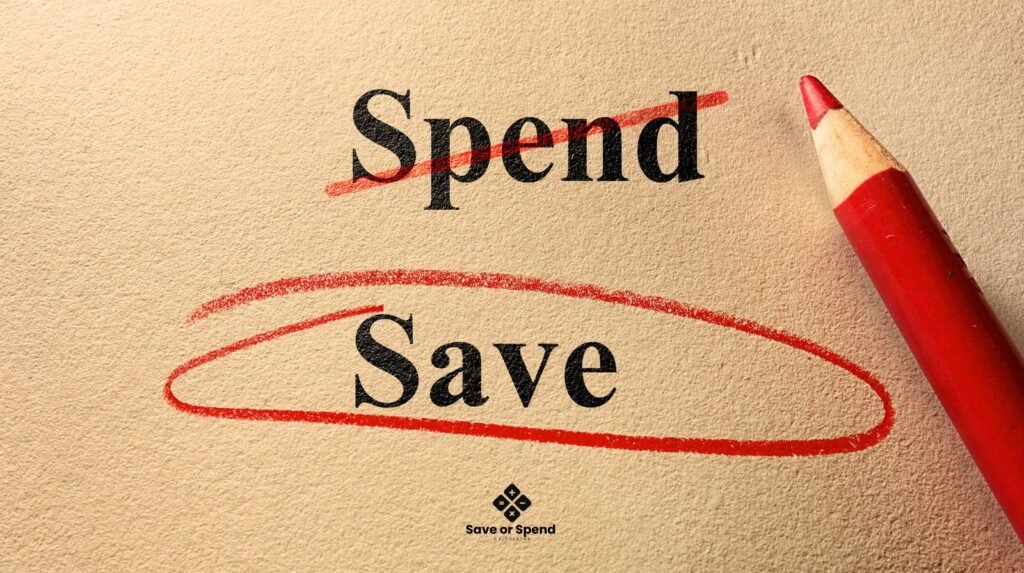

A different way to look at spending

Understanding Opportunity Cost in Everyday Spending

Opportunity cost is the hidden factor behind every spending decision. In simple terms, opportunity cost means choosing one option means giving up another. When you spend money today, you’re not just paying for an item — you’re giving up what that money could have done elsewhere.

For example, if you spend $500 on a purchase, that same $500 cannot go toward savings, emergency funds, debt reduction, or long-term goals. Over time, repeated spending decisions shape your financial flexibility and future options.

This doesn’t mean spending is wrong. It means spending has trade-offs.

Many everyday purchases feel small in isolation. A subscription here, a weekend expense there — each one seems manageable. But when you multiply small decisions across months or years, the cumulative impact becomes significant. Understanding opportunity cost helps you see beyond the immediate price tag and consider the broader picture.

The Save or Spend Calculator makes this concept practical. Instead of thinking only in dollars, it helps translate purchases into effort and time. Seeing what something costs in hours worked can shift your perspective and make trade-offs clearer.

When you understand opportunity cost, decisions become less emotional and more intentional. You can still choose to spend — but you’ll know exactly what you’re choosing over.

When Should You Save Instead of Spend?

Knowing when to save instead of spend isn’t about strict rules — it’s about clarity. There are certain situations where saving creates more long-term benefit than immediate spending.

You may want to consider saving first when:

1. You don’t have an emergency cushion.

Unexpected expenses happen. Building a financial buffer gives you flexibility and reduces stress. Choosing to save instead of spend in these moments protects future stability.

2. The purchase is driven by impulse.

If the desire feels urgent but not essential, pausing can reveal whether the purchase truly adds long-term value or just short-term satisfaction.

3. The expense doesn’t improve your daily life meaningfully.

Some purchases bring ongoing value. Others fade quickly. If the impact is temporary, saving might be the better option.

4. You’re working toward a larger goal.

Whether it’s paying down debt, building savings, investing, or preparing for a life milestone, redirecting spending toward a bigger objective often creates stronger long-term results.

Using a structured decision process — like comparing cost in hours worked — can help remove emotion from the equation. When you see the effort behind the purchase, you can better evaluate whether the outcome justifies the trade-off.

Saving isn’t about deprivation. It’s about alignment. When your money choices reflect your priorities, both spending and saving feel intentional rather than reactive.

When Spending Makes Sense

While saving builds long-term flexibility, spending is not the enemy. In many situations, spending can be the smarter and more meaningful choice.

Spending makes sense when:

1. The purchase improves your quality of life long-term.

If something increases productivity, saves time, supports health, or improves daily comfort, the value may outweigh the cost.

2. It replaces something essential.

Necessary upgrades — like repairing equipment, replacing worn-out tools, or maintaining important systems — are often responsible decisions, not indulgent ones.

3. It supports relationships or experiences.

Some of the most valuable returns in life are not financial. Spending on meaningful experiences, learning opportunities, or connection with others can create lasting benefits.

4. You’ve already planned for it.

If you’ve budgeted for a purchase and it fits within your financial structure, spending can be done confidently and without regret.

The goal of the Save or Spend Calculator is not to discourage spending. It’s to encourage awareness. When you understand what a purchase represents in time and opportunity cost, you can choose freely — not emotionally.

Intentional spending often feels better than impulsive saving. The difference is clarity.

Who this tool is for ?

Informational use only

This calculator is provided for general informational purposes only and is intended to support personal reflection, not to offer financial, legal, or professional advice.

Helpful links

Frequently Asked Questions About the Save or Spend Calculator

Q1: How do I decide whether to save or spend money?

The best way to decide is to evaluate the trade-off behind the purchase. Consider how many hours of work it represents, whether it aligns with your priorities, and what alternative use that money could serve. A structured approach — like using a save or spend calculator — helps remove emotion and improve clarity.

Q2: Is saving always better than spending?

No. Saving builds future flexibility, but spending can improve your present quality of life. The key is intentionality. When spending aligns with your goals and values, it can be just as beneficial as saving.

Q3: What is opportunity cost in simple terms?

Opportunity cost means choosing one option means giving up another. When you spend money on one thing, you cannot use it for something else. Understanding opportunity cost helps you see the real trade-offs behind everyday decisions.

Q4: How can I reduce impulse spending?

Impulse spending often happens when decisions are emotional rather than intentional. Pausing before a purchase, translating the cost into hours worked, and comparing it to your long-term goals can reduce unnecessary spending.

Q5: How do small purchases affect long-term savings?

Small purchases may seem harmless individually, but repeated spending adds up over time. Daily or weekly expenses can accumulate into significant annual totals. Tracking patterns and understanding cumulative impact can improve long-term financial stability.

Q6: Can I use this calculator if I earn a salary instead of hourly pay?

Yes. You can estimate your hourly rate by dividing your salary by total working hours per year, or use your monthly income to approximate the effort behind a purchase. The goal is simply to connect money with effort.

Q7: Does the calculator account for inflation or investment returns?

The calculator provides an estimate based on the inputs you provide. It is designed to offer perspective, not precise financial forecasting. For complex financial planning decisions, professional advice may be appropriate.

Q8: Should I always invest instead of spend?

Not necessarily. Investing can build future wealth, but spending on meaningful experiences, health, or productivity can also provide strong returns. The best decision depends on your priorities and financial position.

Q9: Why does seeing cost in hours make such a difference?

Money can feel abstract, but time feels personal. When you see that a purchase represents several hours or days of work, it often changes how the decision feels. This perspective can reduce emotional buying.

Q10: Is this tool financial advice?

No. The Save or Spend Calculator is for educational and informational purposes only. It is designed to help you think through trade-offs more clearly, not to replace professional financial guidance.

Important Note

The information provided in these FAQs is for general educational purposes only. The Save or Spend Calculator is designed to help you reflect on spending decisions and understand trade-offs, but it does not provide personalized financial advice. Individual financial situations vary, and you should consider your own circumstances or consult a qualified professional before making significant financial decisions.